Look after the pennies and the pounds look after themselves, so goes the saying. Well, the two pence from Citibank have been a source of great amusement to me. And I have a feeling that they have cost everybody involved quite a lot more in time and money. The cashier at NatWest who credited the cheque to my account yesterday had a laugh when I told her the story.

I meant to write a blog post book review of John Lanchester’s Whoops! Why Everyone Owes Everyone and No One Can Pay, so perhaps this will do the job indirectly instead. John Lanchester’s book is about the crazy financial mess we all got into. He starts with a description of what serious, old-fashioned people-facing banks used to do, then explores the Icelandic bank crash and explains how and why our liberal capitalist system has gone so badly wrong.

My tuppence worth backs his analysis up completely.

I returned to England five years ago and was advised by a financial advisor friend to get a credit card for my credit rating, in case I wished to buy property. I did, but with rising prices there was no way that I could afford the most modest property in London. Having lived abroad for twenty years, mainly in France, where personal overdrafts are illegal and the attitude to credit is quite different and more stringently regulated, I had never had a credit card. Not having debt is BAD, said my financial advisor, so I phoned up my bank and they sent me a MasterCard, with a reasonable credit limit. I used it occasionally, but always paid it off so as not to incur any interest charges.

In the summer of 2008, I was going on holiday to Bulgaria, flying with easyJet from Stansted. At the airport, I was accosted by a friendly Liverpudlian lady who offered me an easyJet credit card, which would earn me lots of free air miles, she said. I was reluctant at first, but was in a good mood at the prospect of a holiday in the sun and she was so friendly. She told me that she had promised to take her daughter on a shopping spree to Primark if her daughter cleaned the house while she was out working, i.e. flogging people like me credit cards. So I relented and signed the forms and sure enough, a fancy orange easyJet Citi bank MasterCard arrived in the post. I used it once or twice and they gave me a credit limit of £6,000 immediately. I sometimes day-dreamed about spending that amount all in one go and seeing what happened, but I’m not really a gambler.

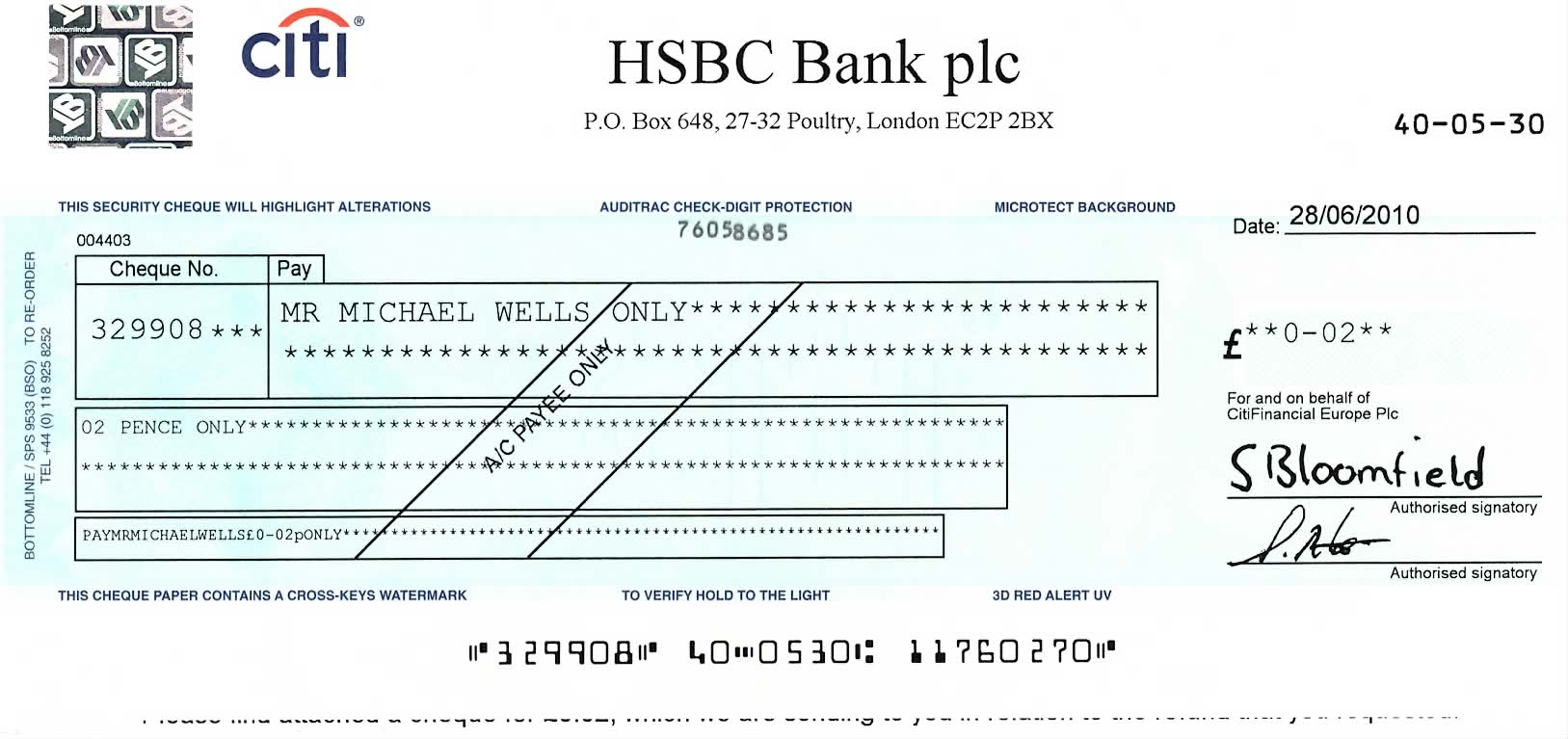

A few air miles accrued, but I preferred to use my other cards, as this one was a hassle to pay off. In November 2009, I received a letter from Citi informing me that they were discontinuing the easyJet MasterCard, but that I would be transferred to a Citi Platinum MasterCard. I could redeem my points or convert them to cash by phoning them up. I got through to a nice lady at a call centre in India who looked at my points and told me that I had lost most of them, as they had expired. However, what was left was worth two pence. We had a laugh about it, but money is money and she credited the 2p to my balance.

A while later my Platinum card arrived. It was silver plastic, really, but nonetheless. Wow, how about that?! Platinum credit, thank you very much. I must say I felt *BIG* wandering around town with a Platinum credit card in my wallet and six grand to splash out.

But bubbles, as they say, burst.

In April this year, I received another letter from Citi telling me that they had transferred their card services to a third party, that I was not included in the transfer and that therefore they were unilaterally closing my account and cancelling the card! So platinum dreams turned to dust.

But the people at Citi bank are good and honest and sent me the cheque for two pence, which is now safely (I hope) in my real bank account.

Whatever the moral of this story, it does seem rather a silly saga of time wasted… Will it affect my credit rating I wonder and if so will that make any difference?

{kind=link}